The smart Trick of Mortgage Lender That Nobody is Talking About

Table of ContentsHome Mortgage Can Be Fun For EveryoneHow Team Quintez - Integrity Home Mortgage Corporation can Save You Time, Stress, and Money.Our Mortgage Lender IdeasA Biased View of Buy A Home

15-year fundings were cheaper at 4. 06%. ARMs were also cheaper, with prices as reduced as 3. 13% readily available. Our rate tables are upgraded daily as well as will reveal you the current prices for your area. There are four core parts of a home loan payment: the principal, interest, tax obligations, as well as insurance, jointly described as "PITI." There can be other prices included in the payment.

If you were to buy a $100,000 home, for circumstances, and obtain $90,000 from a loan provider to assist pay for it, that 'd be the principal you owe. The interest, expressed as a portion rate, is what the loan provider costs you to borrow that cash. In other words, the passion is the annual expense you pay for borrowing the principal.

(In some states, a deed of depend on stands for that safety tool, rather of the home mortgage.) The mortgage's promissory note is what in fact stands for the lending. One more bottom line: While a home mortgage is secured by real estate (simply put, your house), other kinds of fundings, such as bank card, are unsafe, claims Jodi Hall, head of state of Nationwide Home mortgage Bankers, Inc., in Melville, New York City.

The smart Trick of Mortgages That Nobody is Discussing

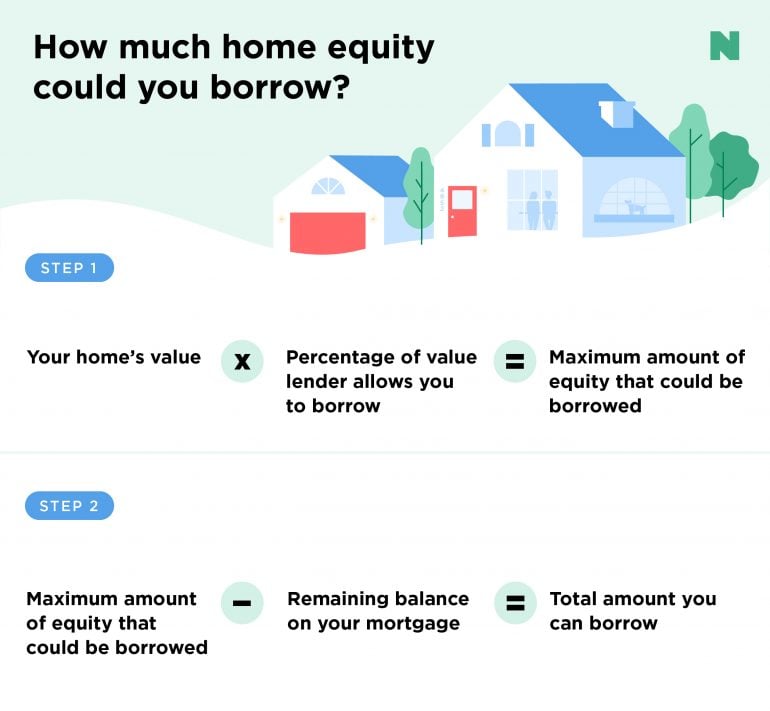

If the residence were to be seized as well as the loan provider offers the residential or commercial property, the proceeds of the sale would first go toward paying off the initial mortgage, because it's in the senior lien placement. A 2nd mortgage refers to a lien in a junior placement, such as a residence equity credit line (HELOC) or house equity lending.

Aim to make every one of your credit report card, car loan or other financial obligation settlements promptly, and check your credit report records for any errors before getting a home mortgage. If you spot incorrect information (like incorrect contact info), dispute it with the credit reporting bureau as soon as possible to get it fixed.

Component of each payment goes toward the principal, or the amount borrowed, while the various other portion goes towards interest.

When a financing fully amortizes, that means it's been paid off totally by the end of the amortization schedule. APR, or annual percentage price, shows the price of obtaining the money for a mortgage. A more comprehensive measure than the rates of interest alone, the APR includes the interest rate, discount points as well as various other costs that come with the financing.

Mortgage Lender Can Be Fun For Everyone

The deposit is the quantity of a home's acquisition cost a buyer pays ahead of time (Mortgage Lender). Customers usually put down see this site a percent of the home's value as the deposit, then borrow the rest in the kind of a mortgage. A bigger deposit can help improve a consumer's opportunities of obtaining a reduced rate of interest.

An escrow account holds the part of a customer's month-to-month mortgage repayment that covers homeowners insurance premiums and go to the website also real estate tax. Escrow accounts also hold the down payment the purchaser down payments between the moment their offer has actually been approved and also the closing. An escrow account for insurance policy and also tax obligations is generally established by the home loan lending institution, who makes the insurance policy and tax repayments on the customer's part.

A home loan servicer is the business that manages your mortgage statements and also all day-to-day tasks connected to managing your lending after it closes. The servicer collects your repayments as well as, if you have an escrow account, makes sure that your tax obligations as well as insurance are paid on time. The servicer also steps in with relief options if you're having problem paying.

/dotdash-111214-buying-home-cash-vs-mortgage-v2-325bbfe3ca7343ca904ecaa9d2cb6c67.jpg)

A home mortgage is likely to be the largest, longest-term finance you'll ever before secure to get the most significant possession you'll ever before own your home - Mortgage Martinsburg. The even more you understand exactly how a home loan functions, the far better equipped you must be to pick the home mortgage that's right for you. A home mortgage is a finance you obtain from a lender to fund a residence purchase.

All About Mortgage Lender

Right here are some common terms you'll require to know if you're getting a mortgage: The cosigned promissory note, or "note" as it is more frequently labeled, details how you will repay the financing, with details including: Your rate of interest Your total car loan amount The term of the financing (30 years or 15 years prevail examples) When the funding is considered late Your regular monthly principal and also rate of interest settlement.

The mortgage provides the loan provider the right to take possession of your home as well as offer it if you do not pay at the terms you concurred to on the note. A deed of count on jobs like a home mortgage as well as is protected versus your residence. Most home loans are contracts in between 2 events you and the lender.

A deed of count on provides the trustee the authority article to take control of your house on behalf of the loan provider if you quit making settlements. These are expenditures billed by a loan provider to make or stem your lending. They commonly consist of source fees, discount factors, costs connected to underwriting, handling, record prep work as well as funding of your financing.

While fees differ extensively by the sort of home mortgage you obtain and also by place, they normally complete 2% to 6% of the loan quantity. On a $250,000 mortgage, your closing prices would amount to anywhere from $5,000 to $15,000. Called "mortgage factors," this is money paid to your loan provider in exchange for a reduced rates of interest.